Small Business Lending Gives a Boost to Banks

By: Carl White

The recession that has accompanied the coronavirus pandemic has hit most sectors of the U.S. economy hard, and commercial banks are no exception. Through the first half of 2020, profits sharply declined from their year-ago levels as banks worked with loan customers through deferrals and modifications, new loan demand fell, and banks set aside more funds for anticipated losses.

Those trends were true of both community banks and their larger counterparts to varying degrees within the District and nationally.

Small Business Lending

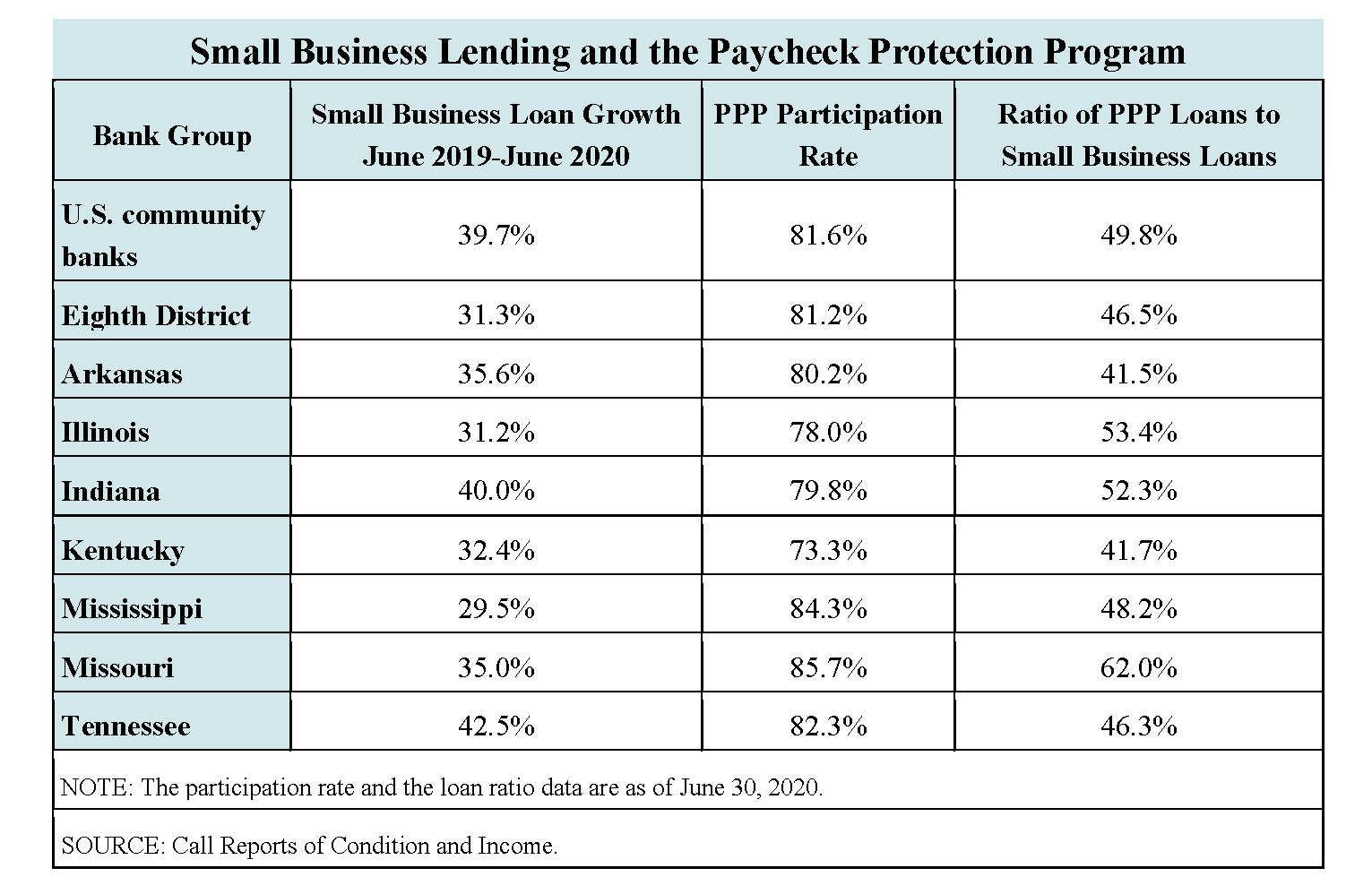

A snapshot of bank health as of June 30 shows one bright spot, however: small business lending.1 Compared with a year earlier, small business loans increased nearly 40% at U.S. community banks. Among all banks in Eighth District states, year-over-year growth ranged from 29.5% in Mississippi to 42.5% in Tennessee, as seen in the table below.

Outstanding loans in every other category—consumer, residential real estate, commercial real estate and agriculture—declined from a year earlier for all U.S. community banks and showed much smaller increases or declines at banks in District states.

The Paycheck Protection Program Boost

The steep increase in small business lending at community banks was spurred by the introduction of the Paycheck Protection Program (PPP), a provision of the Coronavirus Aid, Relief, and Economic Security (CARES) Act passed and signed into law in March. The PPP is administered by the Small Business Administration (SBA) and guarantees the extension of potentially forgivable loans to allow participating employers to keep workers on their payrolls. The maximum loan size is $10 million, and about two-thirds of all loans extended under the program were for $1 million or less.

The vast majority of the nation’s banks have participated in the program. At midyear,

more than 80% of all community banks had extended loans through the program. In the

District, the participation rate was nearly identical and ranged from 73% in Kentucky to

nearly 86% in Missouri.

Although community banks accounted for just 20% of total loans on the books of the

nation’s banks on June 30, they held more than 40% of PPP loans extended by banks.

The average size of a PPP loan was just under $100,000.

The last column of the table shows the ratio of PPP loans to total small business loans.

On average, PPP loans counted for slightly less than half of all small business loan

dollars on the books of community banks at midyear. In District states, the ratio ranged

from 41.5% in Arkansas to 62% in Missouri.

Bump Likely To Be Short-lived

The SBA stopped accepting PPP loan applications in early August. As these loans are paid back or forgiven, the outstanding balance of small business loans will no doubt decline. The outlook for other categories of loans is highly dependent on the size and timing of a rebound in economic activity.

Despite the high participation rates of community banks in the PPP, it’s likely that longterm

trends in small business lending will remain unchanged. Since 2016, community

banks have lagged their larger peers in the extension of small business loans.

Nevertheless, small business lending remains a key business line for community banks,

and it’s highly likely that some new customers who turned to community banks for PPP

loans will stay with these banks. The PPP loan experience may help smaller banks

regain some of the ground they’ve lost to larger competitors in the small business loan

market.

Notes and References

¹ Loans are categorized by the size of the loan and not the size of the business. Of

course, it’s likely that most small loans are made to small businesses. Small

business loans are those that are originated for $1 million or less. Community

banks include commercial banks, thrifts and trust companies with assets of less

than $10 billion.