Stable Funds are more Important than Core Funds

by Donald “Don” Musso

The current regulatory framework for funding and liquidity has some material shortcomings. These shortcomings include: the categorization of digitally originated deposits as noncore, the concern over large balance deposits, the concern over municipal deposits, and the inclusion of listing services as wholesale deposits.

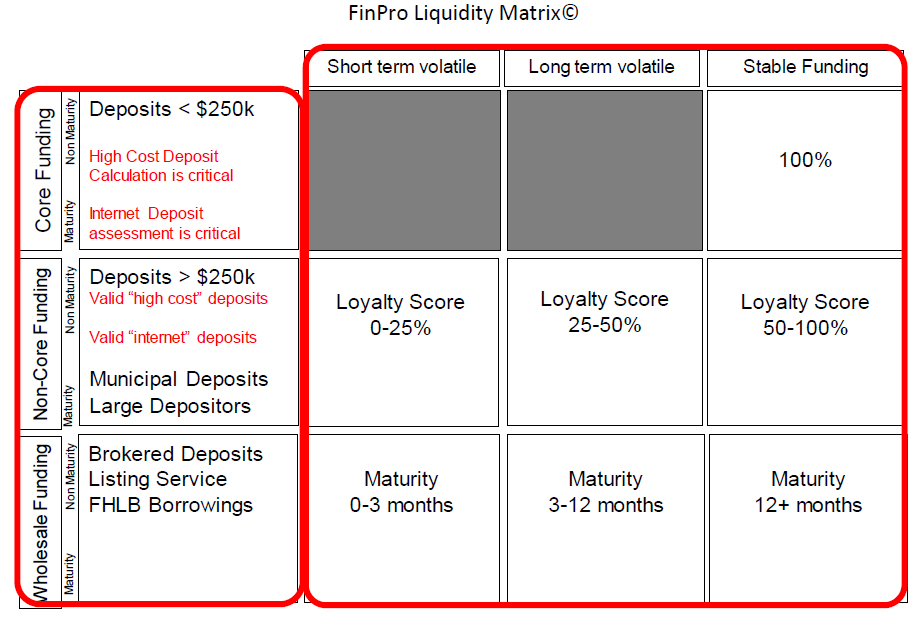

To better assess liquidity risk, banks should establish a matrix that arrays the current regulatory funding categorizations of core, non-core and wholesale against short term volatility, long term volatility and stable funding.

This new matrix arrays the current regulatory designations of funding against deposit stability. This matrix gets to the heart of the risk issue which is the stability of the funding source rather than a generic, non-risk aligned definition like core, noncore and wholesale. Within any of these three categories, funding can be short term volatile (very risky) long term volatile (less risky) and stable (little risk). For example, if a consumer opens a 1 year CD at a 1.00% rate physically in a branch it counts as a core deposit and is considered stable. If that same consumer, the same day, opens another 1 year CD at a 1.00% rate digitally, it would be noncore. Obviously the difference in designation makes no common sense as the funding source is identical.

Not all wholesale funding is risky and/or bad. A wholesale funding source, like a borrowing with a long term maturity, is stable whereas short term maturity is more volatile. The longer the term the more stable the wholesale funding source is.

To determine stability and volatility, banks need to determine customer and account loyalty using an approach similar to the FinPro Deposit Loyalty Score©. This analytical process arrays funding on a grid using stability markers. These stability markers were identified after conducting extensive liquidity analytics at a large number of banks. The markers include, but are not limited to, relationship, transactional activity, digital footprint, age, size, tenure and price. Each marker is assigned a weight based on its relative importance to the specific financial institution.

Each weighted marker has a factor coefficient assigned to it based on institution specific bands. For example, the bands for a marker such as tenure could be less than 1 year, 1 to 3 years, 3 to 5 years and greater than 5 years. The longer the tenure the higher the factor coefficient assigned.

The weighted average result is the loyalty score. The higher the score, the more stable the funding source is as shown in the liquidity matrix.

While the process is complex, the end result is that all accounts have loyalty scores ranging from 0% to 100% that easily reflect their stability within the Bank. Intuitively this makes sense. For example, a large deposit that is from a material owner or family member of an owner, is stable. The size of the deposit itself does not determine volatility or stability. A $1 million dollar deposit from a Board member is much more stable than a deposit from single relationship customer that is less than $250 thousand.

In a similar manner, municipal deposits are not a volatile source of funding simply because they are noncore by regulatory definition. Municipal funding can be arrayed to show balances over time and a minimum threshold can be established that would determine stable funding. For example, if a municipal deposit fluctuated between $1 million and $2.5 million in balance, the first $1 million would be deemed stable and the rest volatile. Additionally, if the municipality is not shopping it’s accounts it could lead to stability. In our municipal example, if the municipality were to not shop the account for another 2 years, the whole balance would minimally be long term volatile.

Listing service deposits should not be deemed volatile either. The vast majority of these deposits are time deposits with identical characteristics to internal bank time deposits. There is no broker involved, rather it is simply digitally originated. As such, listing service deposits should be treated like time deposits.

The Regulatory relief bill started the process of designating funding types to more closely align with true risk. Changing the classification of reciprocal CDARs from brokered to core was an essential first step. It is time to finish the job and align liquidity analytics more closely to reality and true risk.